Sector Rotation Accelerates as Energy and Materials Lead 2026 Rally

Energy and Materials Break Out of Multi-Year Underperformance

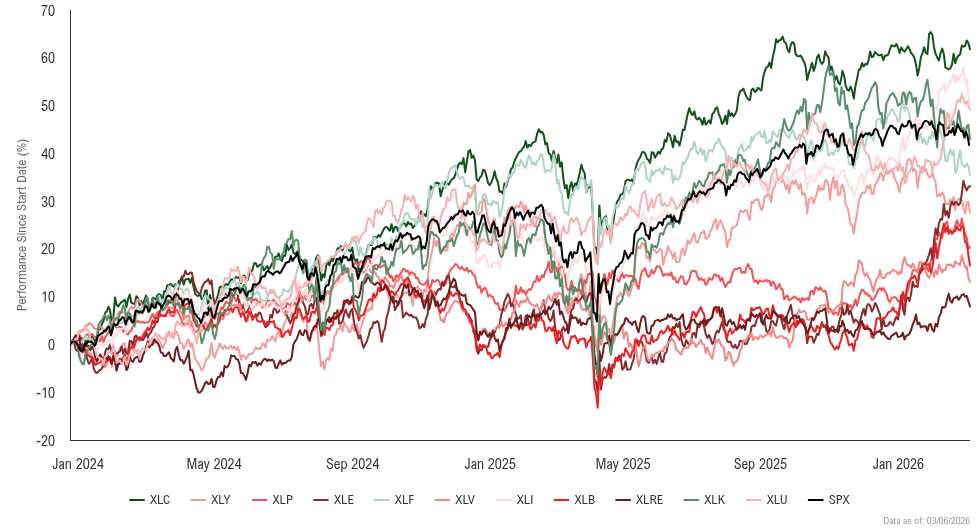

Both Energy and Basic Materials sectors are experiencing a dramatic reversal from multi-year cyclical lows, with our strategists making significant upgrades based on compelling technical and fundamental catalysts [1]. We upgraded Basic Materials from Neutral to Overweight and Energy from Underweight to Overweight. These commodity-related sectors tend to move in sync and are currently reaching cyclical performance troughs versus the broader market [1]. Energy represents a critical structural demand story, highlighted as a "big theme" for AI datacenter power requirements. Technical analysis suggests WTI crude could be ending its three-year bear market with a cyclical bottom expected around February followed by a sharp rally into summer [1].

Early 2026 performance validates our positioning. Both energy and materials stocks have surged more than 9% since the start of the year, far outpacing the S&P 500's 1% gain [2]. This signals the emergence of meaningful sector rotation away from stretched mega-cap technology leadership toward these previously unloved cyclical plays [1][2].

Technology Leadership Shows Signs of Fatigue

Against this backdrop of cyclical sector strength, we have downgraded Technology from Overweight to Neutral as momentum and breadth have declined since July 2025 [1]. The sector has become stretched and overbought across multiple metrics, with countertrend exhaustion signals appearing on weekly, monthly, and quarterly charts [1]. Technology is no longer in an early-cycle phase, which drives our tactical shift away from the sector [1].

However, we see no major issues with the long-term structural trends. Any consolidation would likely create more attractive buying opportunities for selective positions [1]. Our tactical ranking for Technology slipped from #1 to #3, though it remains in our top recommendations [1]. This recalibration reflects the broader sector rotation toward cyclical leadership in Energy and Basic Materials rather than an abandonment of technology's secular growth potential.

Inflation Trends Support Fed Dovishness Despite Market Volatility

The underlying inflation dynamics support our expectation of sustained Fed dovishness through 2026. November's Core PCE details reveal encouraging trends, with hospitals and financial services representing half of the +0.16% month-over-month rise [3]. The financial services component directly links to rising stock prices, raising questions about whether this truly represents problematic inflation pressures. More significantly, the year-over-year Core PCE reading could fall as much as 50 basis points over the next three months due to easier comparisons [3].

This creates a favorable backdrop for the Fed to maintain its dovish stance. Traders now price in a 90% chance of a 50 basis point rate cut at the March FOMC meeting [4]. This dovish pivot provides a critical policy backstop for risk assets through 2026. Fed Chair Powell's recent emphasis on supporting economic growth amid global uncertainties [5] aligns with our view that the central bank maintains a "put" on both the economy and equity markets. Any economic weakness would likely prompt accelerated easing to generate the wealth effect necessary to sustain consumer confidence.