Q1 2026 Market Update: Navigating Rotation, Broadening Leadership, and Volatility

Market Performance: Strong Returns Amid Historic Rotation

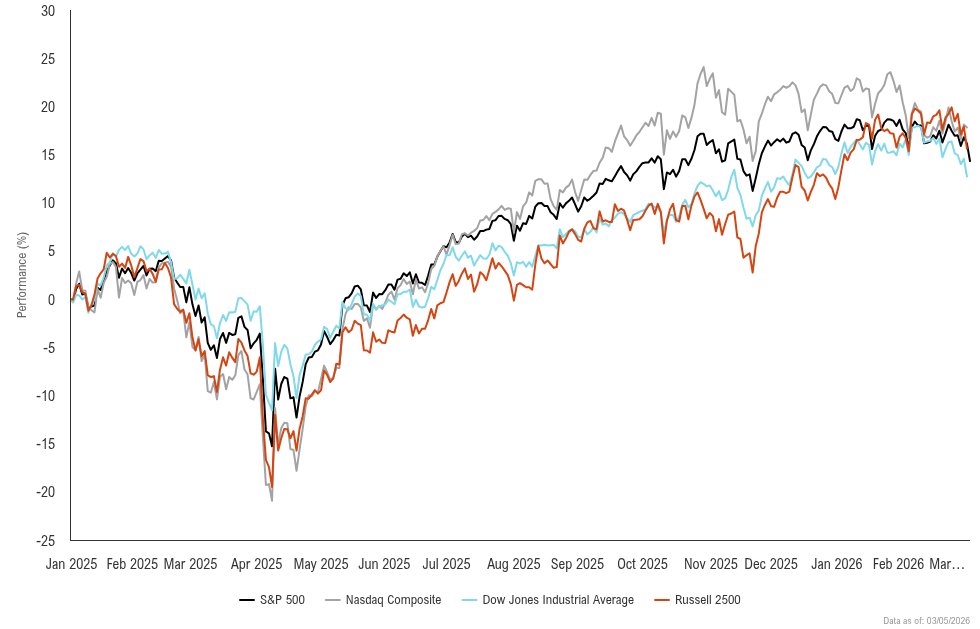

The S&P 500 briefly crossed 7,000 for the first time in late January [1], though two drawdowns followed shortly after. More significantly, the equal-weighted S&P 500 achieved new all-time highs in early February [2] while market-cap weighted indices remained range-bound over a four-month period [3]. In early February, I observed the fourth largest rotation from Growth to Value in over 25 years [2]. Momentum plunged versus value as Big Tech lost leadership to smaller-cap technology and AI-related names. Despite the carnage continuing in parts of Technology, particularly software, it's difficult to call the trend bearish given no material breaks of either the trend from November nor December lows [2]. Broader market breadth has not broken down meaningfully when compared to times of market duress early last year [3], and the S&P 500 has experienced one of its narrowest early-year trading ranges in over 40 years [3]. The Dow Jones Industrial Average, Russell 2000, S&P MidCap 400, and Dow Jones Transportation Average all hit new all-time highs in the past month, while sectors like Materials, Energy and Consumer Staples show stellar signs of outperformance [2][3]. I expect a coming push back to new highs near 7,100-7,200 in the near term. This resilience in breadth indicators and the broadening market participation support my outlook for continued equity strength as rotation creates opportunities beyond mega-cap Growth.

Sector Leadership: Cyclicals and Defensives Gain While Tech Consolidates

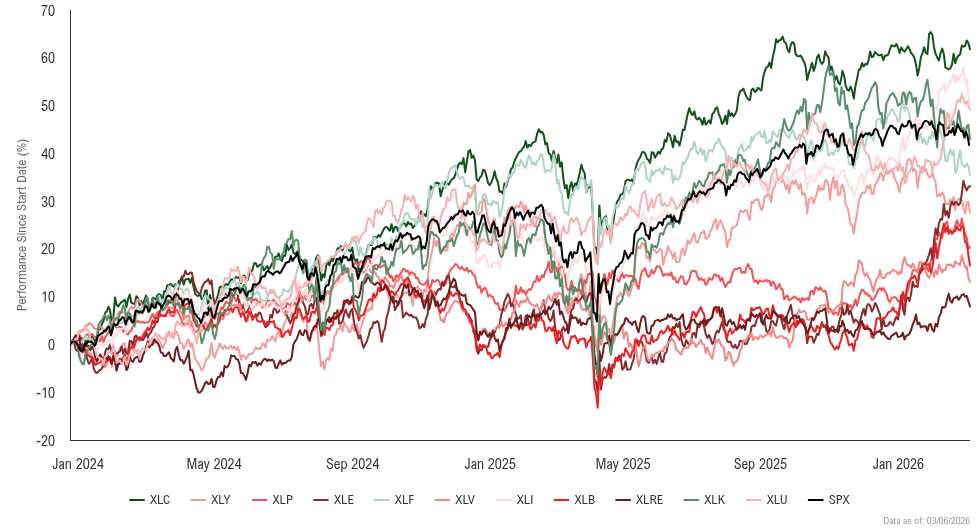

Sector rotation has defined Q1, with cyclicals and defensives gaining ground while Technology consolidates after its extended leadership run. Energy emerged as the top tactical performer with an 18% 30-day return through February [1][4], breaking out versus the Equal-weighted S&P 500 above a multi-year downtrend and climbing from #7 to #1 in tactical rankings. Industrials maintained leadership with the DJ Transportation Average approaching all-time highs—needing just 17 points in early January to eclipse its former record [5]—supported by strength in Aerospace & Defense names and shipping stocks [1]. Financials showed improving technicals, particularly within regional banks, even as the sector experienced bifurcation with mega-cap banks nearing multi-year breakouts while broker-dealers struggled amid crypto-related weakness [6][4].

Technology fell sharply from #3 to #8 in tactical rankings as Big Tech struggled through earnings season, with legacy names losing relevance against newer AI picks and breadth deteriorating across the sector [7][1]. The semiconductor sector showed late-quarter deterioration following NVDA's reversal in late February [8], which broke its uptrend from mid-February and triggered weakness across $SMH and $SOX, though Software is expected to stabilize after significant weakness [6]. Defensive sectors demonstrated surprising strength, with Consumer Staples and Health Care both pushing to new all-time highs in early February [6], prompting an upgrade of Health Care from Neutral to Overweight and Consumer Staples from Underweight to Neutral as these groups show better relative strength heading into spring [1]. This rotation away from mega-cap Growth toward Value, cyclicals, and defensives supports the broader outlook for market participation beyond the narrow leadership that characterized late last year.

What It Means for Long-Term Investors: Embrace Broadening and Stay Diversified

Q1's rotation away from concentrated mega-cap growth reduces single-stock risk and creates opportunities across sectors and market caps [1][3]. In February, I shifted tactical positioning to overweight Industrials, Energy, and Health Care, while maintaining a 0.5% overweight to Technology despite near-term consolidation [1]. The Fed remains dovish—Core CPI printed at 1.6% on a three-month annualized basis through late last year, the lowest level in more than 19 months [9]. I project 15% earnings growth for this year, and ISM Manufacturing broke above 50 after 35 months below that threshold [1]. Volatility and sector rotation will persist, and late-month cycles may pressure markets into March [3]. But the underlying trend holds. I view pullbacks as opportunities, not reasons to exit. Stay diversified across the broadening leadership rather than chasing last year's concentrated winners.