Fundstrat's Top 5 Stock Opportunities: Fundamental Drivers Behind Current Recommendations

Consumer Staples: AI-Resistant Quality with Operational AI Adoption

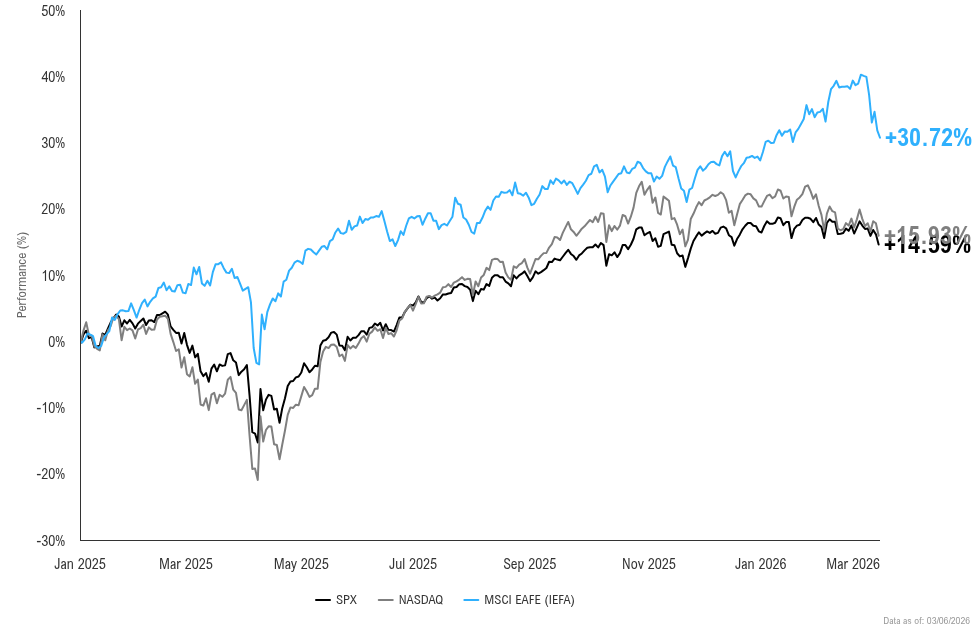

Consumer Staples have surged 15% through February [1] while the information technology sector has declined 4.6%, marking staples' largest outperformance against tech on record according to data going back to 1990 [1]. This rally has pushed staples to trade at 24.60 times forward earnings versus tech's 24.30 multiple, a valuation inversion that has occurred only three other times in the past seven years [1]. The driver is operational AI adoption that enhances rather than threatens these businesses. Walmart's climb to $1 trillion in market value stems from using AI to optimize inventory and sales, with shares up 12% earlier this year [1][2] and contributing significantly to the sector's gains. PepsiCo, up 18% so far this year [1], is partnering with Siemens and Nvidia to deploy AI and digital twin technology that simulates operational changes before implementing them in physical facilities. The sector's core advantage is selling essential household goods regardless of which delivery platform dominates. Combined with a 2.08% dividend yield that exceeds the S&P 500's 1.09% [1], staples offer a defensive growth opportunity with strong fundamental catalysts.

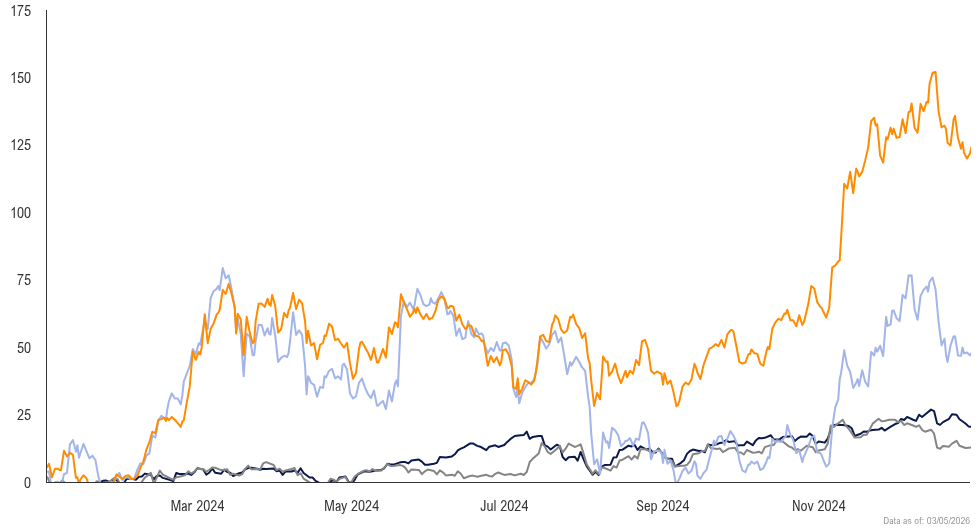

Small-Cap Value Play: Russell 2000 Breakout with AI Infrastructure Beneficiaries

Small-cap stocks have posted 7.8% gains through January compared to just 1.5% for the S&P 500—the Russell 2000's best relative start to a year since 2021 [3]. The valuation discount remains wide: the median Russell 2000 stock traded at 15.48 times forward earnings versus 22.32 times for S&P 500 companies in January [3]. Over the past six months, small-caps rallied 21% against the S&P 500's 11% gain [3]. Specific names show how small-caps capture the same structural themes driving large-cap gains but at cheaper entry points. Bloom Energy surged 60% in January on fuel cell demand for AI data centers, Kratos Defense & Security rallied 64% on defense spending, and Hecla Mining advanced 31% as gold prices strengthened [3]. The breadth of participation across electricity providers, defense contractors, and mining companies suggests durability [3]. Investors are rotating out of stretched Big Tech valuations—the Magnificent Seven underperformed the S&P 500 late last year—while still gaining exposure to AI infrastructure, defense modernization, and commodity strength through small-caps [3][4].

Quantum Computing: IBM's Kookaburra and Government-Backed Innovation Wave

IBM's quantum computing roadmap provides a clear path toward fault-tolerant systems, with the company targeting three critical advances in its 2026 Kookaburr processor: improved fault tolerance, multi-processor linking capability, and quantum memory integration [5]. The company has moved beyond lab demonstrations to test real-world applications in finance, automotive, transportation, and logistics [5]. Its Nighthawk processor already delivers nearly double the coherence of the previous Heron system [5]. Government funding adds substantial support to the investment thesis. In January, the bipartisan U.S. National Quantum Initiative Reauthorization Act called for an additional $2.5 billion in funding [5]. Japan committed ¥1.05 trillion ($7.4 billion) for quantum research through 2030 [5]. The EU allocated an estimated €12.8 billion across various quantum initiatives [5]. IBM's supercooled superconducting circuit approach targets a fully fault-tolerant "Quantum Starling" system by 2029 [5]. The combination of technological milestones, large-scale public capital, and expanding commercial partnerships creates a multi-year growth catalyst, though the technology remains experimental [5].

Financials: Goldman Sachs and AI Infrastructure Lending Boom

Financials offer a compelling opportunity this year, backed by structural tailwinds that position the sector for meaningful upside. Goldman Sachs exemplifies this strength, emerging as the top contributor to the Dow's recent milestone of 50,000 points with shares surging 106% since mid-2024 [2]. The bank's markets division recently posted record annual revenue, partially driven by AI-fueled market activity [2]. Its lending division benefits from surging demand for data center construction financing as companies race to build AI infrastructure [2]. Beyond Goldman, the broader sector shows attractive fundamentals. Mega-cap banks appear on the verge of significant multi-year technical breakouts [4]. Improving conditions for small-caps should provide meaningful support to regional banks that struggled in prior years [4]. We view Financials as a "multiple expansion sector" that should benefit from the Fed's dovish stance. In December, the Fed cut rates and confirmed it is not contemplating rate hikes [4]. The structural demand for AI infrastructure lending represents a multi-year growth driver that should support continued outperformance and justify higher valuations as this year progresses [4].

AI Infrastructure Rotation: Caterpillar and the 'Bullets' Trade

The AI trade is rotating from the Magnificent Seven "armies" toward infrastructure "bullets"—processors, chips, energy providers, and data center builders [6]. The Mag7 now trade at 29.24x forward P/E and have underperformed by 1.9% since last October [6]. Caterpillar exemplifies this shift: shares surged 109% as the machinery maker's engines and generators became critical to data center construction amid power shortages [2]. The company's annual sales growth is expected to reach 5-7% through 2030, up from a historical average of 2.8% [2]. In January, we upgraded Energy from Neutral to Overweight and Basic Materials from Neutral to Overweight, citing persistent shortages in power turbines and the critical role of energy infrastructure in AI expansion [4]. This rotation mirrors the 1990s wireless buildout, when investors alternated between carriers and equipment makers [6]. The pattern creates multi-year structural demand for industrial equipment manufacturers positioned at the intersection of AI infrastructure and energy supply, though the shift between "armies" and "bullets" will likely continue to alternate as it did during the wireless era [6][4].