Labor Market Dynamics: From Resilience to Rotation (2025-2026)

Hard Data Resilience: Employment Strength Defies Survey Weakness

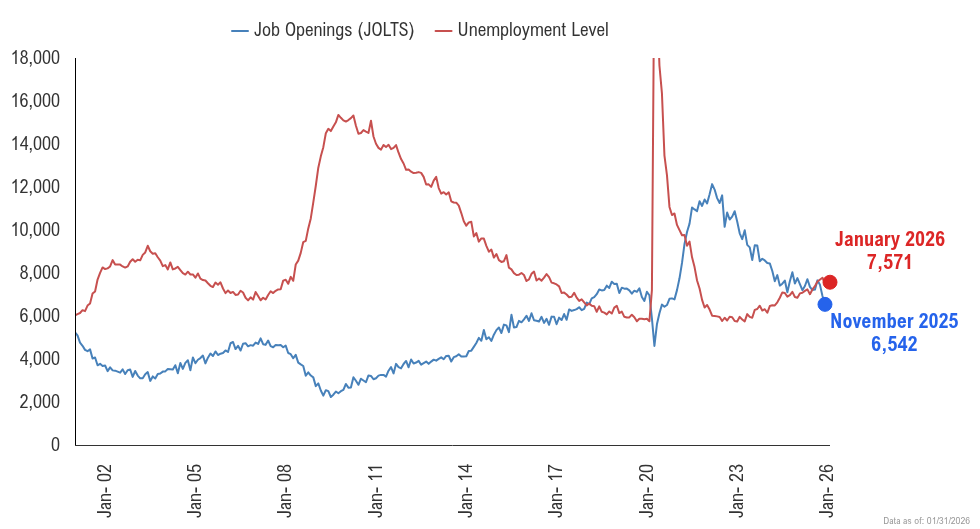

The labor market's resilience through mid-2025 stood in stark contrast to persistent manufacturing weakness, creating a divergence that shaped the Fed's policy stance heading into this year. In June last year, jobs reports and JOLTS data showed unexpected strength [1], even as ISM manufacturing remained below 50 for its 28th consecutive month [1]. Fed Chair Powell explicitly acknowledged this split last March, noting that while soft survey data had weakened, hard employment data maintained its strength—something the Fed was watching closely and did not want to dismiss [2]. This divergence between hard and soft data became a critical factor in the Fed's decision to hold rates steady through much of last year. Policymakers weighed survey-based pessimism against actual hiring and job openings that continued to exceed expectations [2]. The persistence of this pattern through mid-2025 reinforced the view that employment strength would anchor the Fed's cautious approach to rate policy into this year.

Fed Policy Response: Dual Mandate Balance and Rate Path

The Federal Reserve maintained its benchmark rate at approximately 4.3% through Q1 last year, with policymakers in March last year expecting two rate cuts for the year [3][2]. By early this year, inflation pressures had eased considerably. December Core CPI came in at 0.24% versus Street expectations of 0.32%, marking the third consecutive month of softer-than-expected readings. Three-month annualized core CPI reached 1.6% by December—the lowest level in more than 19 months [4]. At the January FOMC meeting, Fed Chair Powell acknowledged that the tension between the central bank's dual mandates of controlling inflation and maximizing employment is "less than it was" [4]. Powell's statement signals the Fed has become less worried about inflation after fighting it since 2022. This shift allows policymakers to refocus attention toward the employment mandate while maintaining a measured approach to rate policy. Macroeconomic conditions remain conducive to equity market strength as the Fed navigates its dual objectives with greater flexibility.

Consumer Spending Bifurcation: High-Income Stress Emerges

Consumer spending through much of last year depended on high-income households, but by early last year, stress appeared even in this segment. Households in the top 10% by income ($250,000 or more) accounted for 49.7% of consumer spending by early last year [5], the highest level recorded since 1989. Credit-card delinquency rates for those earning $150,000 or more doubled between early 2023 and early last year [5]. In March last year, major airlines revised their bullish 2025 forecasts sharply downward—a telling signal given that premium and higher-class seats disproportionately target wealthier travelers [5]. Employment and income pressures were no longer confined to lower-income brackets. The bifurcation in spending patterns—where the affluent had previously offset weakness among lower-income households—was narrowing. We believed labor market health would be critical to sustaining economic momentum into this year.